Money Success vs Debt: The Psychology of Debt You Ignore

Learn the psychology of debt, the hidden mental traps that fuel overspending, and a simple science-backed plan to win money success without shame or stress.

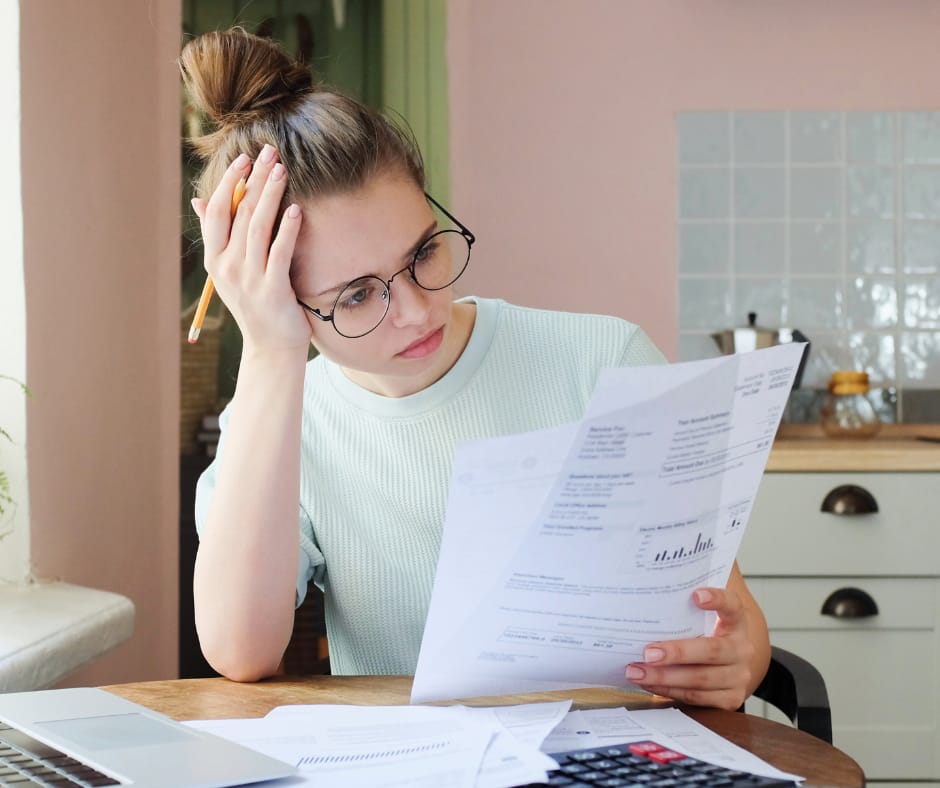

I used to tell myself I was “good with money” because I paid the minimums on time. Then one night, staring at a blinking banking app, I felt the weight of numbers I’d avoided. The balance was not just math, but it was a throb in my chest. If you’ve felt that sting, you’re not weak. You’re human. And the psychology of debt—how our brains react to scarcity, stress, and status—explains why smart people still get stuck. Today, you and I will strip away the fog, face the mental traps head-on, and build a clean, calm plan that turns pressure into power.

The psychology of debt isn’t taught in schools. Nobody warns you that your brain actively works against your financial freedom. Nobody explains why smart, capable people make devastating money choices that contradict everything they know.

We won’t rely on vague advice. We’ll use science: loss aversion, present bias, scarcity mindset, reward loops, and the “pain of paying.” We’ll also add compassion and a bit of tough love. Because money success isn’t just about spreadsheets. It’s stories, habits, and identity. Together, we’ll change all three.

The psychology of debt: why smart people overspend

When money feels scarce, the brain narrows its focus to the crisis in front of you. That tunnel vision, called the scarcity mindset, pushes you toward quick relief—like tapping a credit card—not long-term gain. The psychology of debt says we often spend to soothe stress, not to solve it. Add loss aversion (we fear losses more than we value equal gains), and you get stuck protecting today’s comfort while sacrificing tomorrow’s freedom.

Behavioral psychology of debt and everyday choices

Present bias makes “now” heavier than “later.” You promise to save next month, then reward yourself tonight. The psychology of debt shows how tiny choices—rush delivery, buy-now-pay-later, automatic renewals—chip at your future. Your brain is not broken; it’s wired for short-term wins. We’ll retrain it to prefer small, steady victories over noisy, expensive highs.

Understanding the Psychology of Debt and Your Brain’s Betrayal

Your brain lies to you about money constantly. Understanding these deceptions is crucial for breaking free from the psychology of debt.

Present Bias

Your brain values immediate pleasure far more than future consequences. That new phone feels more real than retirement twenty years from now. Scientists call this temporal discounting, and it’s hardwired into human psychology.

Research from Princeton University shows that when making financial decisions, different parts of your brain compete. The limbic system wants instant gratification. The prefrontal cortex tries to plan for the future. Guess which one usually wins?

Cognitive Dissonance

You know debt is bad, yet you keep accumulating it. This psychological conflict creates mental stress that your brain resolves by minimizing the problem. “It’s not that much.” “Everyone has debt.” “I’ll fix it next month.”

The psychology of debt thrives on these rationalizations. Your mind creates elaborate stories to justify destructive behaviors.

Loss Aversion

Humans fear loss more than they desire gain. This explains why you might continue bad financial patterns rather than face the “loss” of your current lifestyle. The psychology of debt convinces you that cutting back means losing happiness.

Studies show we feel losses approximately twice as intensely as equivalent gains. This means the pain of giving up your $5 daily latte feels more intense than the pleasure of having that $150 monthly savings.

The Hidden Psychology of Debt in Modern Society

We live in a culture designed to keep you in debt. This isn’t a conspiracy theory. It’s calculated psychology.

Credit card companies employ behavioral psychologists to design reward programs that exploit the psychology of debt. They know exactly how to trigger your spending impulses while minimizing payment motivation.

The minimum payment option? Pure psychological manipulation. It lets you feel responsible while ensuring you stay trapped in interest for years.

Social media amplifies the psychology of debt exponentially

You scroll through curated highlights of other people’s lives, their purchases, their experiences. Your brain doesn’t distinguish between reality and performance. You feel inadequate, left behind, missing out.

This Fear of Missing Out (FOMO) becomes a debt sentence. Research from the American Psychological Association found that social media use correlates directly with increased spending and financial stress.

Marketing has become so sophisticated that companies can predict your buying triggers better than you can. They know when you’re vulnerable, when you’re happy, when you’re likely to impulse buy. The psychology of debt isn’t just about your weakness—it’s about billion-dollar industries exploiting human nature.

Money scripts: how childhood writes your spending story

Maybe you grew up hearing “we can’t afford it,” or you saw money used as proof of love or status. These “money scripts” run in the background. The psychology of debt says unexamined scripts predict overspending, avoidance, or hoarding. Name your script: scarcity, status, caretaker, or escape. Once you name it, you can rewrite it.

Read this: Why You Keep Earning More but Saving Less: A Lifestyle Trap

Social comparison: debt dressed up as success

Scrolling past perfect trips and designer gadgets triggers status anxiety. You then spend to match a highlight reel, not a real budget. The psychology of debt shows that comparison lowers contentment and raises impulse buying. Your fix is not zero fun, it’s planned fun with honest trade-offs and clean boundaries.

Immediate concerns: fees, fatigue, and the cost of cluttered attention

Debt isn’t only interest and late fees. It taxes your attention. Decision fatigue drains your energy at work and at home. The psychology of debt links cognitive load to poorer choices—skipping payments, missing due dates, and grabbing fast food because you’re mentally cooked. Reduce the load; your choices improve.

Debt types and mental framing: good, bad, and honest

Don’t fall for slogans. A student loan can be wise or reckless. A credit card can be a tool or a trap. The psychology of debt calls for honest framing: ask, “Does this debt grow my future cash flow or only buy relief?” If it only buys relief, treat it like a fire—contain it fast.

Step 1: Clarity sprint—face the numbers without flinching

Open every account. List balances, APRs, minimums, and due dates. No drama, just data. The psychology of debt predicts that clarity reduces fear because uncertainty is heavier than bad news. Put your list on one page. The mess shrinks when it’s visible.

Step 2: Stabilize cash flow—plug the leaks

Run a 7-day spend log. Tag each cost as need, nice, or numb (impulse). The psychology of debt says awareness alone cuts 10–20% of “numb” spending. Cancel one subscription, renegotiate one bill, switch one habit (brew at home weekdays). Small cuts, repeated, beat heroic budgets that collapse.

Step 3: Choose a payoff path your brain will stick to

Avalanche (highest APR first) saves the most interest. Snowball (smallest balance first) gives quick wins. The psychology of debt favors momentum, so if wins keep you going, pick snowball. If you’re steady, pick avalanche. The right plan is the one you’ll obey on bad days.

Step 4: Automate decisions so willpower can rest

Automation bypasses temptation. Auto-pay minimums to avoid fees. Auto-transfer a fixed extra to the target debt. The psychology of debt shows pre-commitment boosts follow-through. Set “spend-free windows” (e.g., 7 p.m.–7 a.m., no purchases). Fewer decisions, fewer leaks.

Step 5: Rewire rewards—make saving feel like a win

Create a fast feedback loop. Each time you skip a purchase, move that exact amount to a visible “Win Jar” account. Celebrate with a checkmark streak. The psychology of debt tells us that immediate rewards beat delayed promises. Make saving feel tasty now.

Step 6: Build an emergency buffer so debt stops roaring back

Even a $300 buffer lowers panic. The psychology of debt links safety to better choices. When life hits, you won’t sprint back to the card. Treat the first $1,000 as a non-negotiable wall between you and chaos.

Step 7: Identity shift—“I am the kind of person who…”

Lasting change is identity-based. Say, “I am the kind of person who plans purchases.” The psychology of debt shows identity drives habit selection. Your rules become simple: delay 24 hours, compare three options, and never finance a feeling.

The psychology of debt in relationships: money fights, silent shame

Debt breeds secrecy and blame. One partner guards receipts; the other plays parent. The psychology of debt says shame shuts down problem-solving. Use weekly 20-minute “money huddles”: one metric, one win, one fix. Small, calm, consistent.

Work, income, and the psychology of debt: earning without lifestyle creep

A raise helps only if lifestyle stays steady. The psychology of debt warns about hedonic adaptation—new comforts become normal fast. Pre-decide: for the next raise, 70% goes to debt, 30% to joy. Enjoy, but don’t torch momentum.

Scripts that break the spell when you want to splurge

-

“If I buy this, what do I say no to?”

-

“Will future-me thank me or curse me?”

-

“Is this relief or a real need?”

These questions exploit the psychology of debt by slowing impulse and invoking loss aversion in your favor.

Read this: Your Debt Doesn’t Define You — But Your Next Move Will

Practical Steps to Overcome the Psychology of Debt

Understanding the psychology of debt means nothing without action. Here’s what actually works.

Create a debt map

List every debt with its emotional charge, not just its balance. Which debts cause the most shame? Which ones trigger the most anxiety? Attack these first, regardless of interest rates. The psychology of debt is eliminated through emotional victories, not just mathematical ones.

Implement the 24-hour rule

When you want to buy something, wait 24 hours. This simple pause interrupts the psychology of debt’s instant gratification loop. Your prefrontal cortex gets time to engage, and impulsive purchases decrease dramatically.

Build a zero-judgment awareness practice

Track your spending for 30 days without criticism. Just observe. The psychology of debt weakens when you remove shame from the equation. You can’t change patterns you won’t acknowledge.

Create friction for spending

Delete saved credit card information from websites. Leave your cards at home and use cash. Make spending slightly inconvenient. The psychology of debt relies on effortless transactions.

Celebrate small wins

Your brain needs positive reinforcement. Each time you resist an impulse or make a debt payment, acknowledge it. This releases dopamine and strengthens new neural pathways, weakening the psychology of debt over time.

Seek community

The psychology of debt thrives in isolation. Find others working on financial freedom. Share your struggles. Celebrate their victories. Human connection provides neurological regulation that individual willpower cannot.

Emotional punchlines to remember when it’s hard

You don’t owe brands your peace.

Debt is loud; freedom is quiet.

Small wins, stacked daily, crush “someday.”

The psychology of debt explains your past, not your future.

Advanced levers: friction, defaults, and environment design

Add friction to spending: remove saved cards from browsers, turn off one-click, and set a 24-hour delay rule. Remove friction from saving: payroll splits, default transfers, and round-ups. The psychology of debt respects the environment more than intentions. Design the room; shape the result.

Dealing with emergencies without detonating your plan

When life hits—car repair, medical bill—pause extra payments, not minimums. Use the buffer first, then resume. The psychology of debt teaches us that flexible plans survive. Rigidity breaks; resilience bends and returns.

What to do this week: a 7-day sprint to real momentum

-

Day 1: List every balance and APR.

-

Day 2: Set auto-pay minimums and one extra transfer.

-

Day 3: Cancel one subscription; renegotiate one bill.

-

Day 4: Create “Win Jar” and move the first skipped spend.

-

Day 5: Pick snowball or avalanche; commit in writing.

-

Day 6: Plan a joy that costs <$10; prove joy ≠ swipe.

-

Day 7: Hold a 20-minute money huddle (solo or with partner).

By the end, the psychology of debt shifts—from panic to control.

Common traps and how to crush them fast

-

Trap: Emotional sales events. Solution: pre-decide a tiny fun budget.

-

Trap: Buy-now-pay-later stacking. Solution: allow only one active plan, ever.

-

Trap: “I deserve it.” Solution: You deserve peace more. Delay 24 hours.

-

Trap: Complexity. Solution: one page, one number to beat this month.

Final thought: money success is quiet power

Debt thrives in the dark. Shine light on it with simple rules, automatic moves, and tiny rewards that feel good now. The psychology of debt no longer manipulates you; you use it to your advantage. You’re not behind—you’re just getting accurate. Begin today, and keep going when it’s boring. That quiet is freedom.

Frequently Asked Questions

What is the psychology of debt, in simple words?

It’s how your brain and emotions shape money choices—especially under stress. The psychology of debt explains why you may overspend for relief and avoid hard numbers.

Is a snowball or an avalanche better for paying debt?

Avalanche saves more interest; snowball builds faster motivation. The psychology of debt favors the one who keeps you consistent. Pick and stick.

How do I stop impulse buys?

Add friction: remove saved cards, set a 24-hour rule, and keep a “Win Jar.” The psychology of debt responds to small delays and visible wins.

Can I still have fun while paying off debt?

Yes—pre-plan low-cost joys. The psychology of debt improves when joy is scheduled, not swiped in panic.

What if I feel ashamed of my balance?

Shame is common and unhelpful. The psychology of debt shows clarity, and small wins reduce shame fast. Start with one number and one action.